Your dream of building a lasting family legacy shouldn't be held hostage by the fear of complex spreadsheets or predatory interest rates. Many aspiring entrepreneurs stall at the starting line because they view capital as a barrier rather than a strategic tool for growth. It's natural to feel a sense of anxiety when you're weighing the risks of using your retirement savings or trying to decipher the latest SBA requirements.

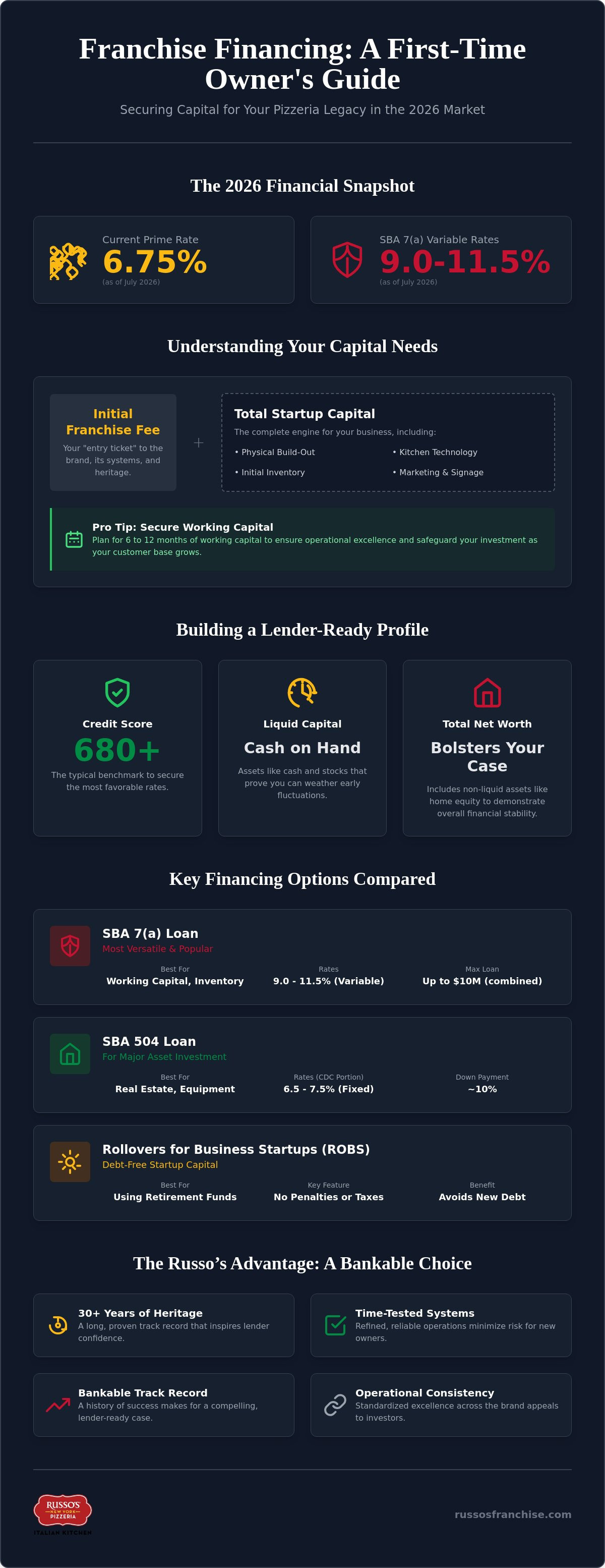

We believe that a clear path to ownership is built on transparency and professional discipline. This guide clarifies the landscape of Franchise Financing Options for First Time Owners , showing you how to secure capital without compromising your financial peace of mind. With the current Prime Rate at 6.75% and SBA 7(a) variable rates ranging from 9.0% to 11.5% as of July 2026, the right strategy can transform a daunting investment into a stable, high-performance reality.

You'll find a comprehensive breakdown of funding sources, from the newly increased $10 million SBA loan limits to the strategic nuances of Rollovers for Business Startups (ROBS). We provide the roadmap you need to qualify for competitive rates and approach your chosen brand with the confidence of an investor who knows exactly how to build a bankable future.

Key Takeaways

- Distinguish between your initial franchise fee and the total startup capital necessary to maintain operational excellence during your first twelve months.

- Master the complexities of Franchise Financing Options for First Time Owners by leveraging government-backed SBA programs designed for stability.

- Unlock creative funding strategies, such as Rollovers as Business Startups (ROBS), to invest in your future without incurring early withdrawal penalties.

- Build a compelling, lender-ready business case by emphasizing the time-tested reliability and operational consistency of your chosen brand.

- Discover how the Russo’s Advantage—rooted in thirty years of culinary heritage—provides the bankable track record lenders find most attractive.

Navigating the Initial Investment Landscape in 2026

Capital is the lifeblood of any culinary legacy. When you step into the world of premium restaurant ownership, you aren't just buying a job; you're investing in a refined, time-tested system. Success requires a clear-eyed understanding of the difference between the initial franchise fee and your total startup capital. The franchise fee is your entry ticket, granting you access to the brand's intellectual property and heritage. However, your total startup capital represents the entire engine, including the physical build-out, kitchen technology, and the necessary inventory to serve your first guest.

The 2026 market presents a unique environment for those exploring Franchise Financing Options for First Time Owners . With the Prime Rate holding at 6.75% as of July 2026, lenders have sharpened their criteria, looking for partners who demonstrate both financial discipline and a deep commitment to operational excellence. Viewing debt as a strategic tool rather than a burden is a vital psychological shift. In the hands of a disciplined owner, well-structured financing isn't just a loan; it's the leverage needed to scale a tradition of quality across multiple units.

Determining Your Total Capital Requirement

Precision is the hallmark of a professional business plan. You must account for every detail, from leasehold improvements and high-grade pizza ovens to the initial marketing blitz that announces your arrival. The Franchise Disclosure Document (FDD), specifically Item 7, serves as your essential guide, offering a transparent range of expected costs. Under-capitalization remains the primary risk for new owners. To safeguard your investment, it's prudent to secure 6 to 12 months of working capital. This reserve ensures you can maintain meticulous standards and retain a top-tier team while your customer base grows.

The Role of Personal Net Worth and Liquidity

Lenders prioritize stability. When evaluating small business financing options, they look closely at your liquid capital, which includes cash, stocks, and other assets that can be quickly converted. While non-liquid assets like home equity can bolster your overall net worth, banks often require a specific threshold of "cash on hand" to ensure the business can weather early fluctuations. For premium restaurant financing in 2026, a credit score of 680 or higher is typically the benchmark for securing the most favorable rates. This financial foundation reflects the same discipline you'll bring to the kitchen, proving to partners that you're ready to uphold a legacy of success.

Government-Backed and Traditional Loan Structures

Securing the right capital is as much about timing as it is about creditworthiness. For those exploring Franchise Financing Options for First Time Owners , the U.S. Small Business Administration provides a safety net that traditional lenders often require for new ventures. These SBA-guaranteed loans reduce the risk for the bank, allowing you to access higher leverage and longer repayment terms. In the current 2026 climate, where variable rates for 7(a) loans hover between 9.0% and 11.5% APR as of July, choosing a program that aligns with your specific growth goals is essential for long-term stability.

Lenders value stability. While the interest rate environment has stabilized compared to previous years, the cost of debt remains a primary consideration for your monthly overhead. Mastering the financial landscape means understanding that a loan is more than just a transaction; it's a partnership between your vision and the bank's appetite for risk. A disciplined approach to your loan structure today sets the stage for a legacy that will thrive for decades.

SBA 7(a) vs. 504: Which Fits Your Pizzeria?

The 7(a) program remains the most versatile instrument for launching a new location, covering everything from initial inventory to essential working capital. If your vision includes purchasing the property or investing in high-capacity Italian kitchen equipment, the 504 loan offers a more stable, fixed-rate structure for the CDC portion, which currently ranges from 6.5% to 7.5%. As of July 2026, the SBA has increased the combined loan limit for 7(a) and 504 programs to a maximum of $10 million for qualified entrepreneurs. While the 504 typically requires a 10% down payment, the 7(a) application timeline can take several months, demanding patience and meticulous documentation from the borrower.

Conventional Lending for Italian Kitchen Models

Conventional debt remains a powerful option for those with significant liquidity or established business histories. Local community banks often look favorably upon candidates who choose a pizza & Italian kitchen franchise with a 30-year track record of success. These institutions value the reliability of a proven model over a government guarantee, though they typically require a higher down payment of 20% to 30%. Building a relationship with a commercial loan officer early in your search is vital. They don't just see numbers on a page; they see the person behind the brand and the potential for a successful, multi-unit partnership that honors a tradition of quality.

Creative Financing: Leveraging Existing Assets

Not every path to ownership begins at a bank teller's window. For those seeking Franchise Financing Options for First Time Owners , the most powerful capital might already be under your control. Leveraging your own assets allows you to maintain greater equity while launching a brand built on heritage and quality. Expert franchise funding advice often points toward these creative avenues to bridge the gap between liquid cash and total investment. By looking inward at your existing portfolio, you can often find the flexibility needed to scale a business without the immediate pressure of traditional debt servicing.

Portfolio-based lending is another sophisticated tool for the modern entrepreneur. This allows you to use your stocks, bonds, or mutual funds as collateral for a line of credit. Unlike selling your positions, which could trigger capital gains taxes, this method keeps your investments intact while providing the liquidity needed for a premium build-out. Similarly, a professionally structured "Friends and Family" round can provide a warm start. We recommend treating these as formal business transactions with clear legal agreements to protect both your personal relationships and your growing legacy.

ROBS: Debt-Free Financing Without Tax Penalties

Rollovers as Business Startups (ROBS) offer a disciplined way to fund your vision using existing retirement accounts. This IRS-recognized method allows you to use your 401(k) or IRA funds to buy a franchise without incurring the standard 10% early withdrawal penalty or immediate income taxes. To remain compliant, you must establish a C-Corporation and a new 401(k) plan for that entity. While setting this up typically costs between $4,000 and $5,000 in initial fees with a monthly administration fee around $139, it provides a debt-free foundation. It is vital to understand that if the business fails, you risk losing the retirement savings you've invested in the company's stock.

Equipment Financing and Leasing Strategies

High-CAPEX items like traditional brick ovens and professional-grade Italian kitchen technology don't always need to be purchased upfront. Leasing these essential tools is often a smarter move in 2026, as it preserves your cash flow for marketing and initial operations. This approach also allows you to utilize Section 179 tax deductions, which can let you write off the full purchase price of qualifying equipment in the year it's put into service. This strategic move significantly improves your pizza franchise ROI by reducing your tax liability during the critical first year of growth. By preserving your liquid capital for operational excellence, you ensure that every guest experiences the quality your brand represents from day one.

Building a Lender-Ready Business Case

Approaching a lender is a moment of high-level professional presentation. You aren't just asking for capital; you're inviting a financial partner to participate in a legacy of growth. When researching Franchise Financing Options for First Time Owners , many entrepreneurs focus solely on their personal credit score, yet the strength of your chosen brand is often the deciding factor in a bank's risk assessment. A lender-ready business case blends hard data with the narrative of a time-tested model, proving that your success is a natural outcome of following a refined path.

Preparing your package involves five critical steps to ensure your application stands out in the 2026 lending environment:

- Step 1: Craft a business plan that centers on brand stability and local market demand.

- Step 2: Compile three years of personal and professional tax returns to demonstrate financial discipline.

- Step 3: Develop a detailed pro forma that projects revenue and expenses for the first 36 months.

- Step 4: Secure a formal Letter of Intent (LOI) from your franchisor to show a committed partnership.

- Step 5: Present the "Heritage Factor"—the unique operational history that ensures your location isn't a gamble.

The Power of a Proven Business Model

Banks crave predictability. A franchise with over 30 years of history, such as Russo's, offers a safe harbor for capital that new, unproven concepts cannot match. In your profit and loss projections, quantifying the value of "scratch-made" dough and proprietary family recipes demonstrates a competitive moat that generic brands lack. This isn't just about culinary quality; it's about a differentiator that drives customer loyalty and consistent average unit volume. You can see how these metrics stack up against the competition in this pizza franchise comparison 2026, which provides the market research lenders need to see.

Operational Strategy as Financial Security

Your financial projections are only as strong as the operations behind them. Lenders want to see that you won't be navigating the industry alone. By detailing your training schedule and the franchisor's support network, you prove that operational risks are minimized by a refined blueprint. Additionally, a rigorous site selection strategy—utilizing data-driven demographics and high-traffic mapping—shows the bank that your location is chosen for performance. Ultimately, investing in a proven Italian kitchen franchise model reduces lender risk by providing a standardized, high-quality experience that has already succeeded in diverse international markets. Ready to build your bankable future? Explore our franchise opportunity and start your journey toward ownership today.

Why Russo’s New York Pizzeria is a Bankable Choice

Choosing to Own a Russo's New York Pizzeria & Italian Franchise - Pizza Franchise Opportunity transforms your loan application from a speculative request into a sound business proposal. Lenders prioritize stability, and our advantage is rooted in a history that dates back to 1992. Because our model has been refined over decades, we provide the operational consistency that banks require for long-term financing. When you explore Franchise Financing Options for First Time Owners , the heritage of the brand you choose acts as a powerful endorsement of your future performance.

We understand that every entrepreneur’s capital journey is unique. Our diverse development models, ranging from traditional full-service Italian kitchens to efficient "slice bar" footprints, provide flexible entry points that align with different investment levels. This flexibility is a significant asset during the underwriting process. Our partners gain access to a dedicated network of preferred lenders and financial consultants who are already familiar with our average unit volume of over $1,081,577. This internal support system streamlines the path to approval, ensuring you spend less time chasing paperwork and more time perfecting your craft.

Founder-led mentorship is the cornerstone of our financial success. Anthony Russo’s hands-on involvement ensures that the original family recipes and high standards for quality remain unchanged, protecting the brand equity that lenders value. This leadership provides a safe harbor for capital, as it guarantees that the business blueprint you follow is the same one that has yielded a reported average net income of 18.25% for our franchised locations.

Heritage and Stability as Collateral

The "New York Style" pizzeria category remains a recession-resistant staple in the global market. Lenders view this longevity as a form of intangible collateral, knowing that premium pizza and authentic Italian cuisine maintain steady demand regardless of economic shifts. This stability is particularly evident in the bankability of our halal pizza franchise models, which allow owners to capture high-growth markets with a specialized, inclusive menu. By leveraging the brand equity found when you Own a Russo's New York Pizzeria & Italian Franchise - Pizza Franchise Opportunity , first-time owners often find themselves in a stronger position to negotiate favorable interest rates and repayment terms.

Your Next Steps to Ownership

The journey toward building your legacy begins with a disciplined capital strategy. We invite you to request our latest Franchise Disclosure Document (FDD), which provides the transparency your financial advisor needs to validate your investment. Once you've reviewed the numbers, scheduling a discovery call will allow us to discuss your specific goals and connect you with our financial support network. Your ambition deserves a proven foundation. Take the first step today and Explore Russo’s Franchise Opportunities to see how our heritage can fuel your entrepreneurial future.

Launching Your Future with Financial Confidence

Mastering the financial landscape is the first step in transforming an ambitious vision into a tangible legacy. You now have the roadmap to navigate Franchise Financing Options for First Time Owners , from leveraging government-backed SBA programs to utilizing creative asset-based strategies like ROBS. By building a lender-ready business case that highlights both your personal discipline and a brand's proven stability, you position yourself as a partner rather than just a borrower.

At Russo’s, we offer more than just a business model. We provide a foundation built on 30+ years of proven profitability and globally recognized authentic recipes. Our founder-led training and support ensure that you're never navigating the complexities of ownership alone. This unique combination of heritage and operational excellence creates the consistency that modern lenders demand, making your path to approval smoother and more predictable.

Your journey toward ownership starts with the right information and a disciplined plan. Download Your 2026 Franchise Financial Starter Kit to begin refining your capital strategy today. We're ready to help you build a future that honors tradition while driving sustainable growth. Welcome to the family.

Frequently Asked Questions

What is the minimum credit score needed for a pizza franchise loan in 2026?

A credit score of 680 or higher is the standard benchmark for securing the most favorable rates for a restaurant loan in 2026. While some specialized lenders may consider scores as low as 640 with significant collateral, a higher score demonstrates the financial discipline required to manage a premium Italian kitchen model. Maintaining a strong credit profile is essential for proving your reliability to potential banking partners.

Can I use a 401(k) to fund my first Russo’s New York Pizzeria?

You can utilize your 401(k) or IRA through a Rollover as Business Startup (ROBS) to fund your dream when you decide to Own a Russo's New York Pizzeria & Italian Franchise - Pizza Franchise Opportunity . This method allows you to invest your retirement savings into your own business without incurring early withdrawal penalties or immediate taxes. It provides a debt-free foundation, allowing you to focus on the operational excellence and heritage-driven growth that defines our brand.

How much liquid cash do I need to qualify for SBA financing?

Lenders typically require first-time owners to possess liquid cash equal to 10% to 20% of the total initial investment to qualify for SBA financing. This ensures you have sufficient "skin in the game" and a safety net for your first twelve months of operations. For those exploring Franchise Financing Options for First Time Owners , having this liquidity ready is a prerequisite for a successful application.

Does Russo’s New York Pizzeria offer direct in-house financing?

While we don't provide direct in-house lending, those who Own a Russo's New York Pizzeria & Italian Franchise - Pizza Franchise Opportunity benefit from our deep relationships with preferred third-party lenders. These financial partners are well-versed in our business model and historical performance, which often streamlines the underwriting process. We act as a guide, connecting you with consultants who understand the specific needs of a premium Italian kitchen investment.

Is it better to lease or buy kitchen equipment for a new pizzeria?

Leasing kitchen tech is often the smarter choice for a new location because it preserves your liquid capital for marketing and essential working capital. In 2026, leasing allows you to benefit from Section 179 tax deductions while ensuring your kitchen stays equipped with the latest high-performance technology. Preserving your cash flow during the initial growth phase is vital for long-term operational success.

How long does the franchise financing approval process typically take?

The approval process generally takes between 60 and 120 days depending on the loan type and the complexity of your business plan. SBA loans typically reside on the longer end of this spectrum due to federal documentation requirements and government-backed guarantee procedures. Starting your financial preparations early ensures your capital is ready the moment you've secured your ideal restaurant site.

What are the main differences between SBA 7(a) and SBA 504 loans?

The SBA 7(a) is a versatile loan used for working capital, inventory, and equipment, whereas the SBA 504 is specifically designed for long-term fixed assets like real estate. Both are excellent Franchise Financing Options for First Time Owners , but the 504 often offers lower, fixed interest rates for the CDC portion of the loan. Your choice depends on whether you intend to lease or purchase your physical location.

Can first-time owners qualify for multi-unit development financing?

First-time owners can qualify for multi-unit financing if they demonstrate significant liquidity and a sophisticated management plan. Lenders look for evidence that you can scale a proven model while maintaining the high standards of a premium brand. A multi-unit agreement often requires a more detailed pro forma that shows how you will manage the operational complexities of multiple territories simultaneously.